There Is A Court Date already scheduled For Your Accounts.

You Can Stop It.

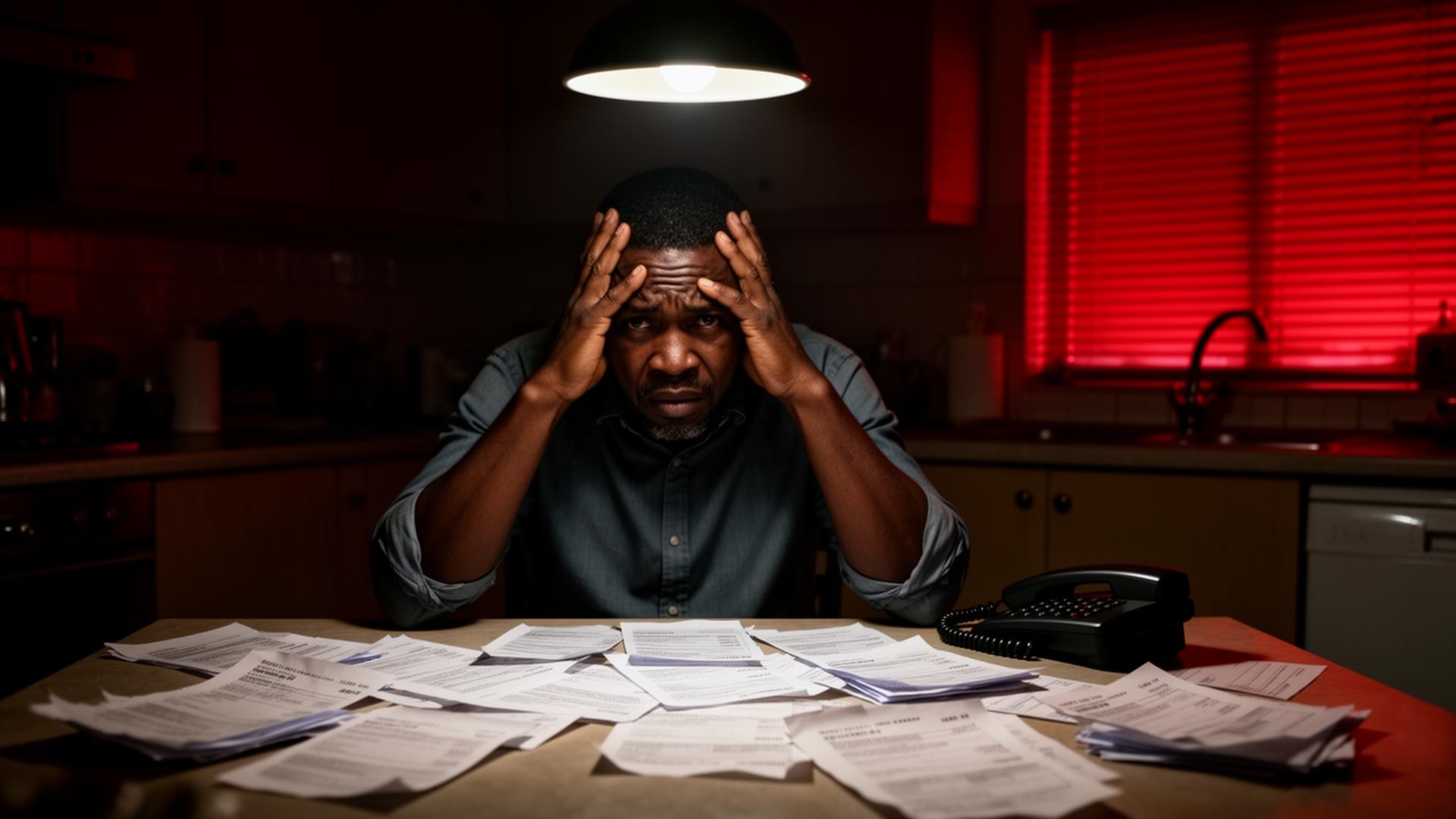

If you have missed payments on credit cards, personal loans or store accounts, your creditors are already preparing legal action. Section 86 of the National Credit Act gives you 7 days to act first — and we file it for you.

- 01Freeze creditor calls and legal action within 5 working days

- 02Cut combined monthly repayments by up to 60%

- 03Protect your car, your home and your salary from attachment

Free · No obligation · Takes 60 seconds

A piece of South African legislation, passed in 2005, exists for exactly this.

If any of this sounds like your life right now, you are not alone — and you are not beyond help.

The latest Consumer Credit Market Report shows that 1 in 3 credit-active South Africans is three months or more behind on at least one obligation. The vast majority of them are not careless people. They are working adults whose income simply stopped covering the cost of staying alive.

- 01Your salary hits your account on the 25th and is gone by the 27th — most of it to debit orders you can't stop.

- 02You are using one credit card to make the minimum payment on another. The maths stopped working months ago.

- 03Your phone rings from numbers you no longer answer. The dread starts before you even read the screen.

- 04You have received a Section 129 letter, or a summons, or both — and you do not know what either one actually means.

What almost no one tells you is that South African legislation exists specifically to protect you from this situation. Restructuring is a legal right, not a favour. The problem is that most people only learn about it after a sheriff has already knocked on the door.

Free · No obligation · Takes 60 seconds

See the number before you ever sign anything.

Move the sliders. The estimator below shows a worked example of what a restructured monthly instalment could look like, using accepted affordability guidelines. Your written, line-by-line breakdown comes on the first call.

- Indicative only — your specialist confirms the rand value

- No credit check is performed

- Based on standard affordability assessment

Indicative estimate · Standard fees apply

A debt relief practice built on one idea: show the client the full number before they sign.

RedLine Debt Rescue was founded in Sandton in 2020 by debt relief specialist Naledi Khumalo, after a decade inside two of South Africa's largest credit providers. She had watched too many clients sign restructuring agreements without ever seeing what would actually happen to their first three months of payments.

Every RedLine file is opened, managed and closed by a single named specialist. There is no call centre. The person you speak to on day one is the same person who walks you through the final clearance at the end of the process. That is the structural difference.

Before you commit to anything, you receive a written, month-by-month breakdown showing exactly how every rand of your consolidated payment is split between statutory fees and your actual creditors. No surprises in month four. No discoveries on a bank statement.

Five steps from drowning in debt to walking out clear.

The Honest 15-Minute Call

Your dedicated debt expert walks through your income, your accounts and your essential expenses. You get a straight yes or no on whether the programme is right for you — at no cost and no obligation.

Your Written Repayment Plan

Before you sign anything, you receive a month-by-month breakdown showing how your single consolidated payment is split between statutory fees and each creditor.

Application & Legal Protection

Your formal application is lodged with the relevant authorities. Creditors are notified. The Magistrate's Court order makes your new repayment plan legally binding on every credit provider.

One Payment, Distributed For You

Each month one consolidated payment goes to a registered Payment Distribution Agent, who pays every creditor on your behalf at the court-approved amount.

You Walk Out Debt-Free

When your restructured accounts are settled, your clearance is finalised, the flag is lifted from every credit bureau, and your profile is restored.

Free · No obligation · Takes 60 seconds

Real South Africans who started here and got their lives back.

"R287,000 across three credit cards and a Wesbank vehicle finance. My monthly repayments were R11,400. RedLine restructured everything into a single payment of R5,200. Sixteen months in and I have two accounts already settled."

"The sheriff had already served papers on me for an African Bank loan. RedLine had the matter halted within nine days of my first call. I will never forget what that felt like."

"My husband and I were paying R19,800 a month across nine accounts between us. We were borrowing from family to cover groceries. One joint application later we pay R8,400, and three accounts are already done."

"I phoned three other companies first. Two would not give me a fee breakdown without a signed mandate. RedLine emailed mine the same afternoon. That is when I knew."

"Forty-one months. One person looking after my file the whole way through. I got my clearance in February and the flag was off my bureau within three weeks."

"R164,000 in retail and personal loan debt cut down to a payment I can actually live with. I should have done this two years sooner."

"I had stopped opening my post. RedLine took the file, contacted every creditor, and inside two weeks the phone stopped ringing for the first time in a year."

"Professional, honest and they did exactly what they said they would do on the first call. Eleven months in and I am ahead of schedule."

"Truworths, Edgars, Mr Price, Foschini — all of it consolidated into one debit order of R2,100 a month. I cannot describe the relief."

Free · No obligation · Takes 60 seconds

RedLine vs. the industry standard vs. doing nothing.

| What matters | RedLine | Industry Standard | Doing Nothing |

|---|---|---|---|

| Written fee breakdown before sign-up | Provided on day one | Disclosed after signing | No structure |

| Specialist continuity | One named person, start to finish | Rotating call-centre agents | No representation |

| Legal protection from creditors | Active from day of application | Active from day of application | None |

| Court order timeline | Within statutory timelines | Often delayed by months | Not available |

| Creditor calls | Routed through your specialist | Routed through your specialist | Continue indefinitely |

| Track record | 318 successful completions | Volume-driven and inconsistent | Self-managed only |

Free · No obligation · Takes 60 seconds

Four signs the programme was built for you.

Your minimum payments add up to more than you take home.

You have cut subscriptions, stopped eating out, and moved money between accounts to keep the urgent debits alive. The maths still does not work. That is structural over-indebtedness — and the law was written specifically for it.

You dread answering your phone.

Creditors and debt collectors are legally required to stop contacting you the moment your restructuring application is formally submitted. That protection is statute, not a courtesy.

You have a car, a home or a salary you cannot afford to lose.

Asset attachment, vehicle repossession and emolument (salary) attachment orders are all real consequences of unmanaged default. A restructured plan halts every one of them — provided you apply before enforcement begins.

You are formally employed and earn a regular income.

Debt relief is designed for people who can afford to repay their debt, just not at the current contractual rate. If you earn a salary, you almost certainly qualify for restructured terms.

Free · No obligation · Takes 60 seconds

Every month you wait, the numbers get harder to fix.

This is not a sales tactic — it is the legal and mathematical reality of unmanaged default.

- Risk 01

Outstanding balances continue to compound at the contractual rate every month you delay.

- Risk 02

Once a creditor issues a formal demand and ten business days have elapsed, they may file for judgment.

- Risk 03

Once judgment is granted, your assets can be attached and a sheriff can be instructed — and legal protection cannot be applied retrospectively.

- Risk 04

Emolument Attachment Orders (garnishee) can deduct up to 25% of your salary at source, before you ever see it.

One 15-minute conversation changes nothing except how much you know about your own situation. That is all the first step is.

Free · No obligation · Takes 60 seconds

Three commitments we make before you sign anything.

No breakdown, no signature.

You will see the full, written, month-by-month payment plan before you sign anything. If we cannot show it to you, you do not owe us a decision.

One person, named, with a direct number.

From your first call to the day you walk out clear. No call-centre transfer. No 'someone will get back to you'.

An honest answer, even if it is no.

If the programme is not the right tool for your situation, we will tell you so on the first call and point you to what is.

Free · No obligation · Takes 60 seconds

Frequently asked, honestly answered.

You do not have to decide anything today.

You just have to find out where you actually stand. One 15-minute conversation. No documents. No credit check. No obligation to proceed.

Free · No obligation · Takes 60 seconds